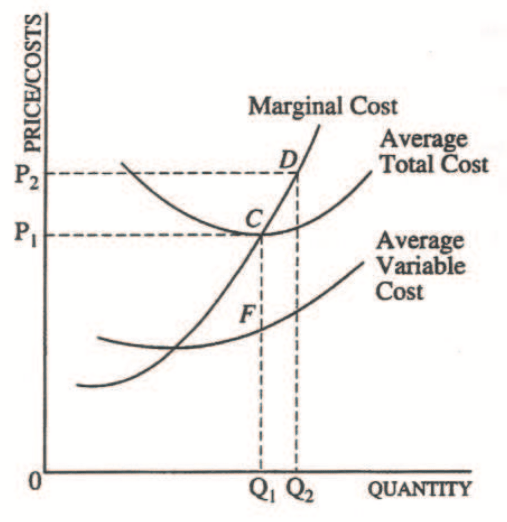

Question 7

A firm will always produce where MR = MC, therefore the firm will produce Q1 units of output.

The firm will produce the efficient level of output since it is producing where P = MC = minimum ATC.

The firm is achieving both allocative and productive efficiency.

The firm will earn a normal profit (0 economic profit) since P = ATC.

This also tells us that total revenue equals total costs when the firm produces Q1 units of output.

The firm will not increase production in the long run since it is already in equilibrium.

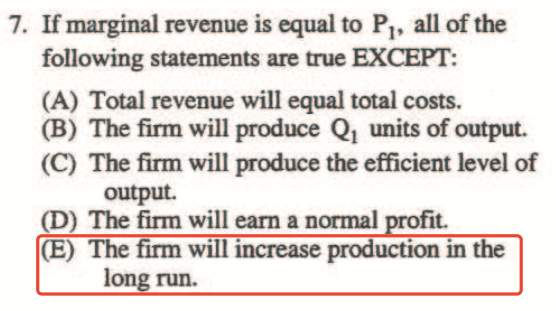

Question 10

For a monopolist at the profit-maximizing output level, the demand curve will not intersect the supply curve

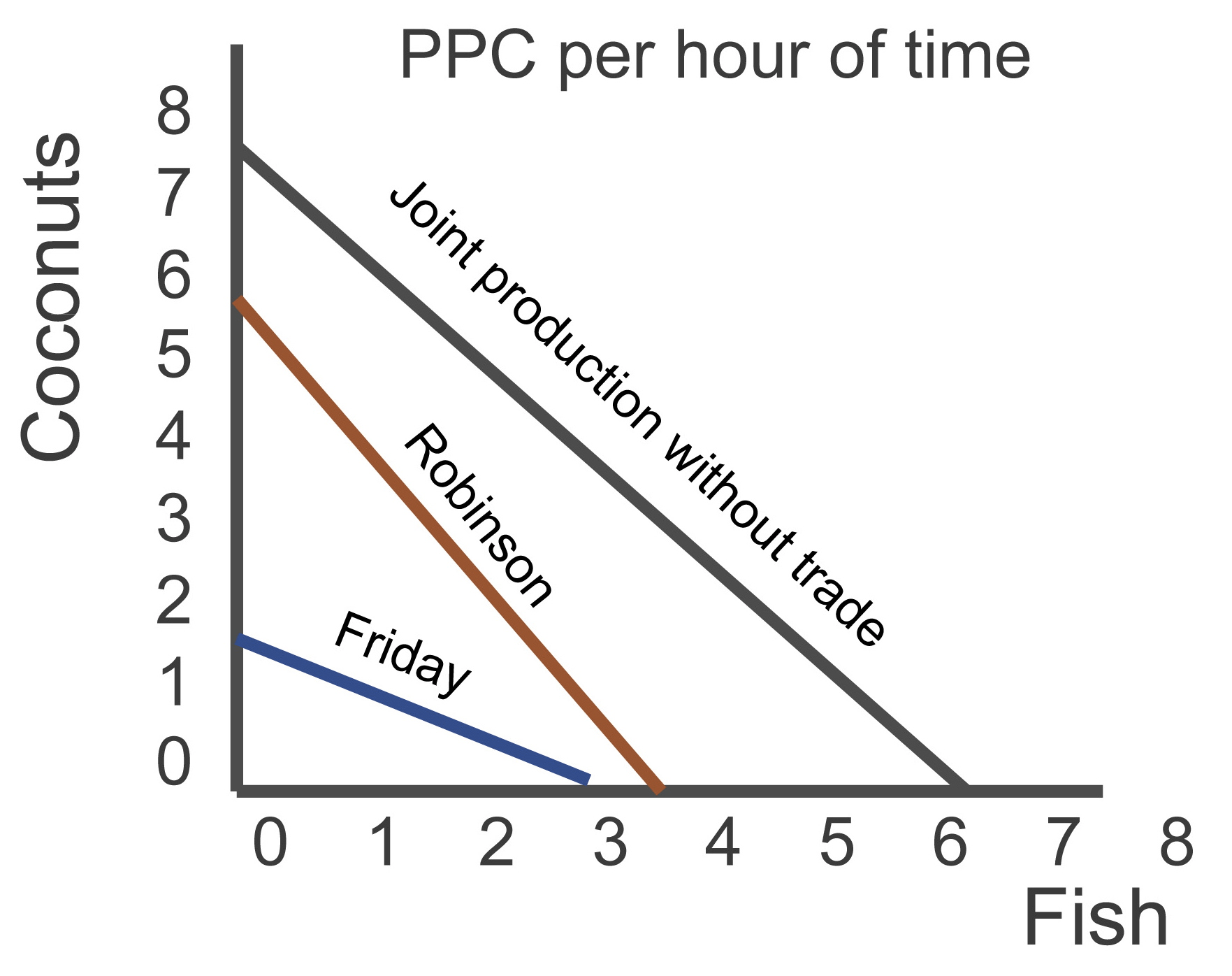

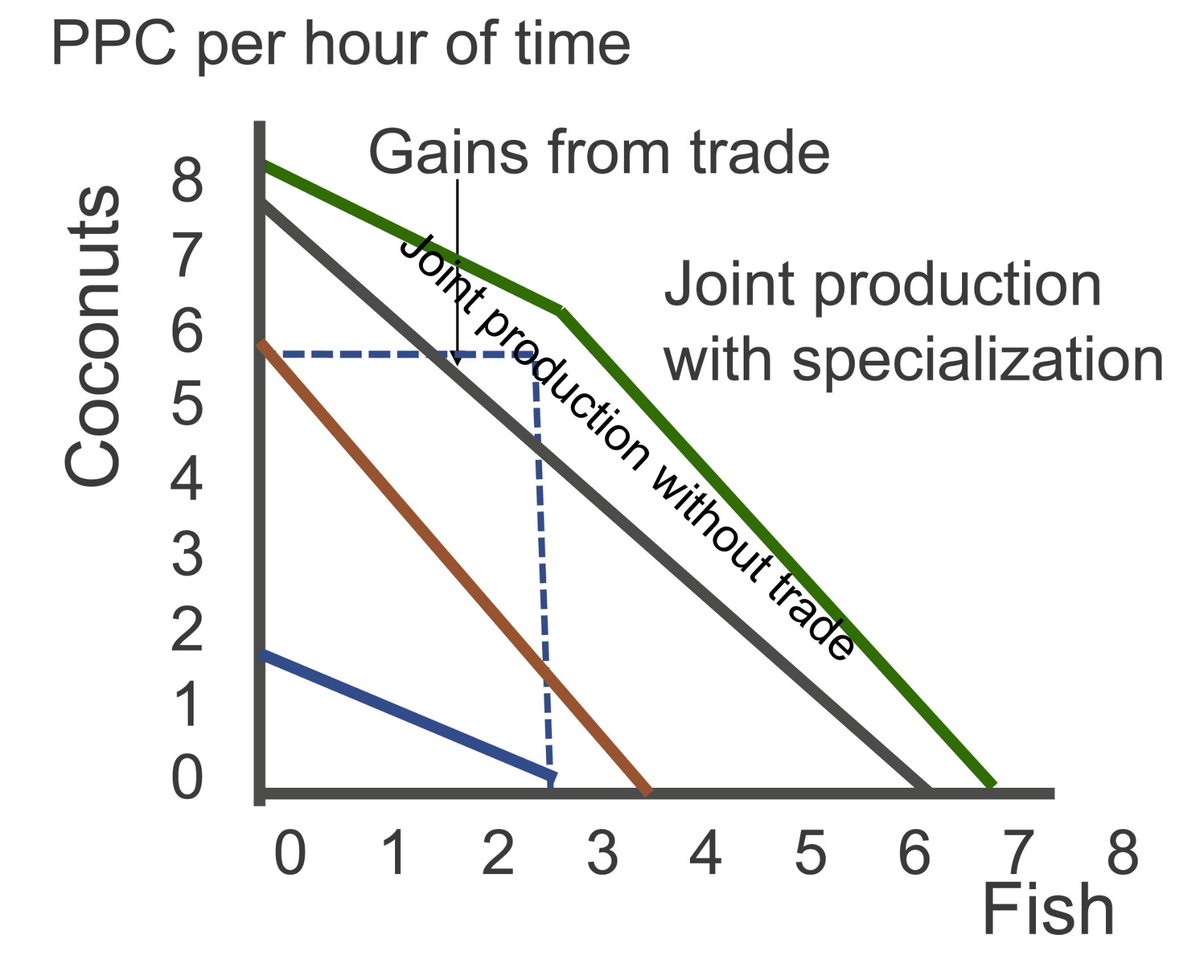

Question 17

Trade is one way for a country to expand its PPC curve since specialization through trade allows for greater efficiency.

Other than trade, a country would have to discover a new supply of resources or technological advancement to shift its current PPC curve.

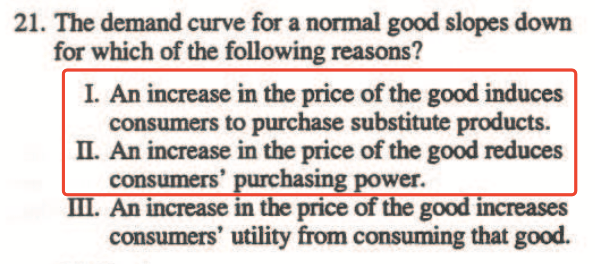

Question 21

- As the price of a good increases, consumers are going to turn to substitutes because the higher price reduces the consumers’ purchasing power.

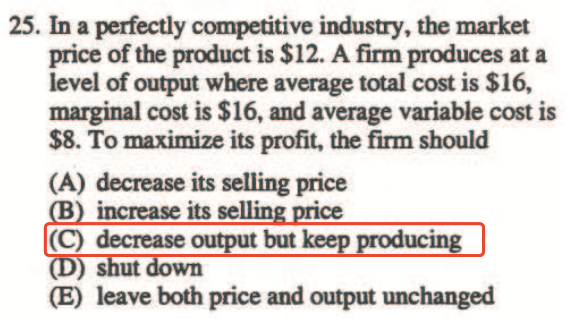

Question 25

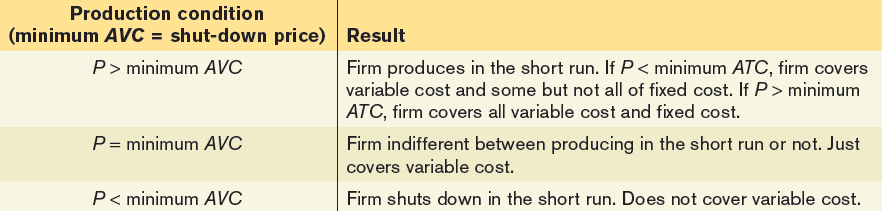

A firm should always produce where MR = MC.

In this situation, the firm is currently producing where MR < MC since $12 < $16.

The firm should decrease output until its MC = $12 and it should keep producing because at that price, P > AVC since $12 > $8.

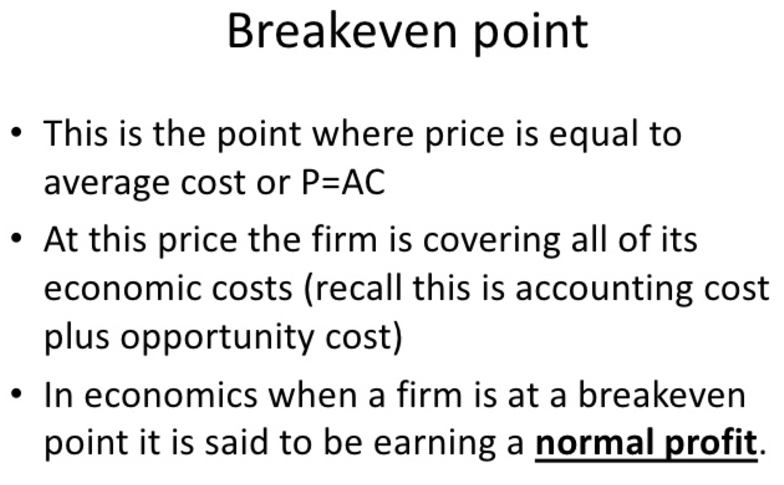

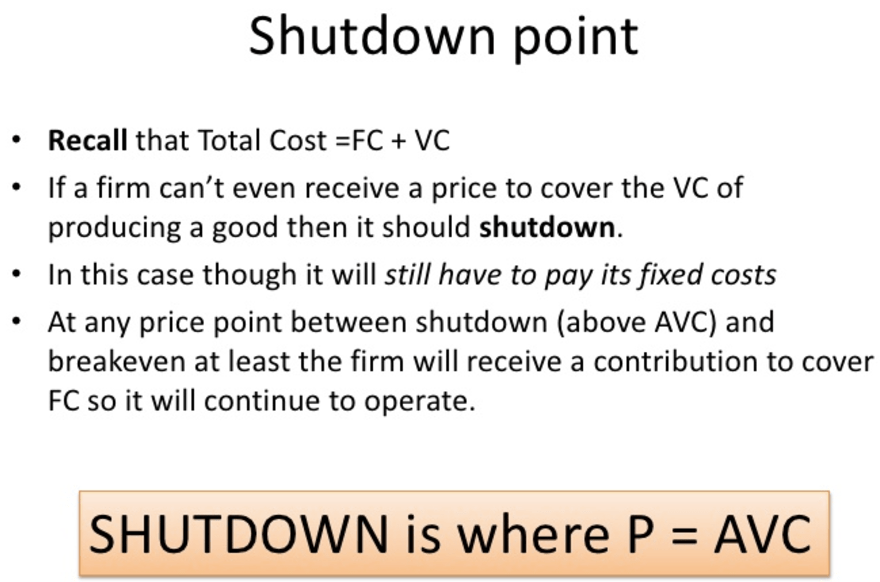

Breakeven vs. Shut down

Long-run (Profitability)

Short-run (Production)

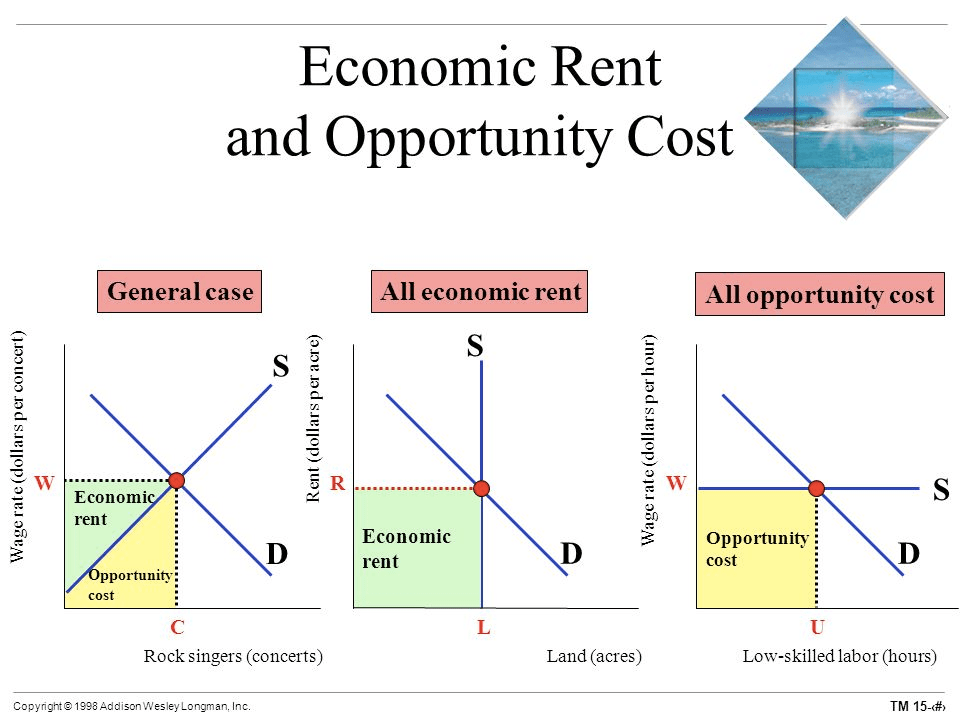

Question 29

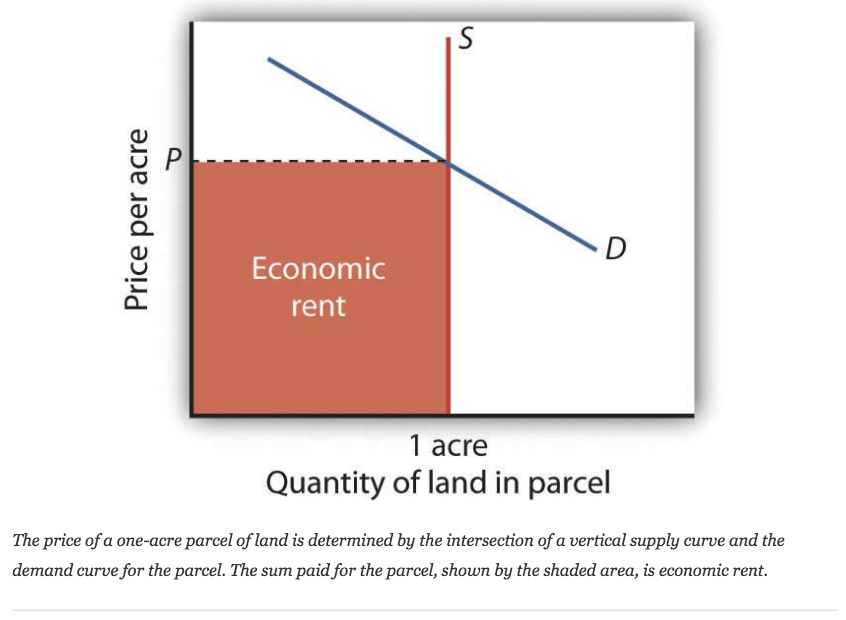

Economic rent is a surplus payment.

If supply is perfectly elastic, there will never be any economic rent.

Economic Rent and Opportunity Cost

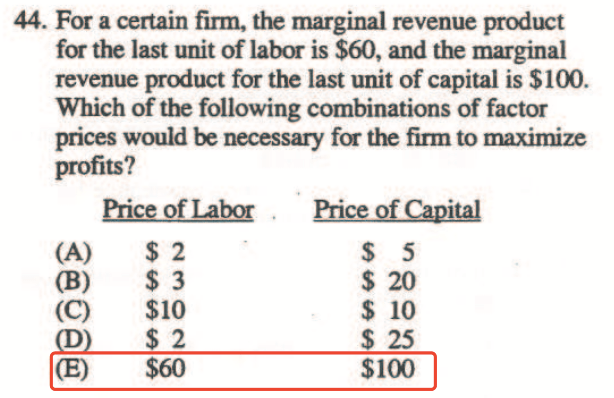

Question 43

Question 44

The profit-maximizing rule states that the MRP/P of each resource unit must equal 1.

In order for that to occur, the price of labor must be $60 and the price of capital must be $100 so that each ratio is equal to 1.

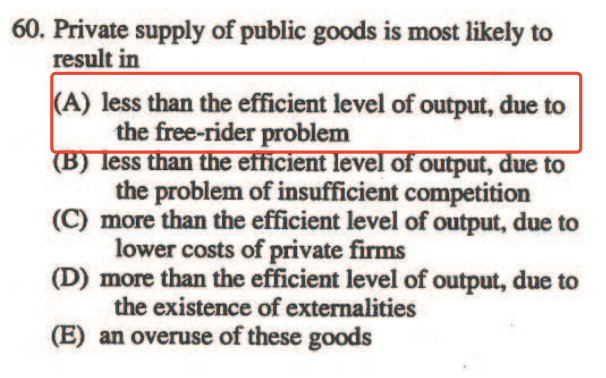

Question 60

Remember, one of the main reasons why we have public goods is due to the free-rider problem.

When you can’t exclude everyone from using a good or paying for its benefits, less than the efficient level will be provided if a private firm is producing that good simply because they need to cover their costs.

A privately produced good may provide additional benefits to others who aren’t paying for the good, yet since the firm doesn’t reap those benefits, they choose to produce less than the efficient amount.