Question 5

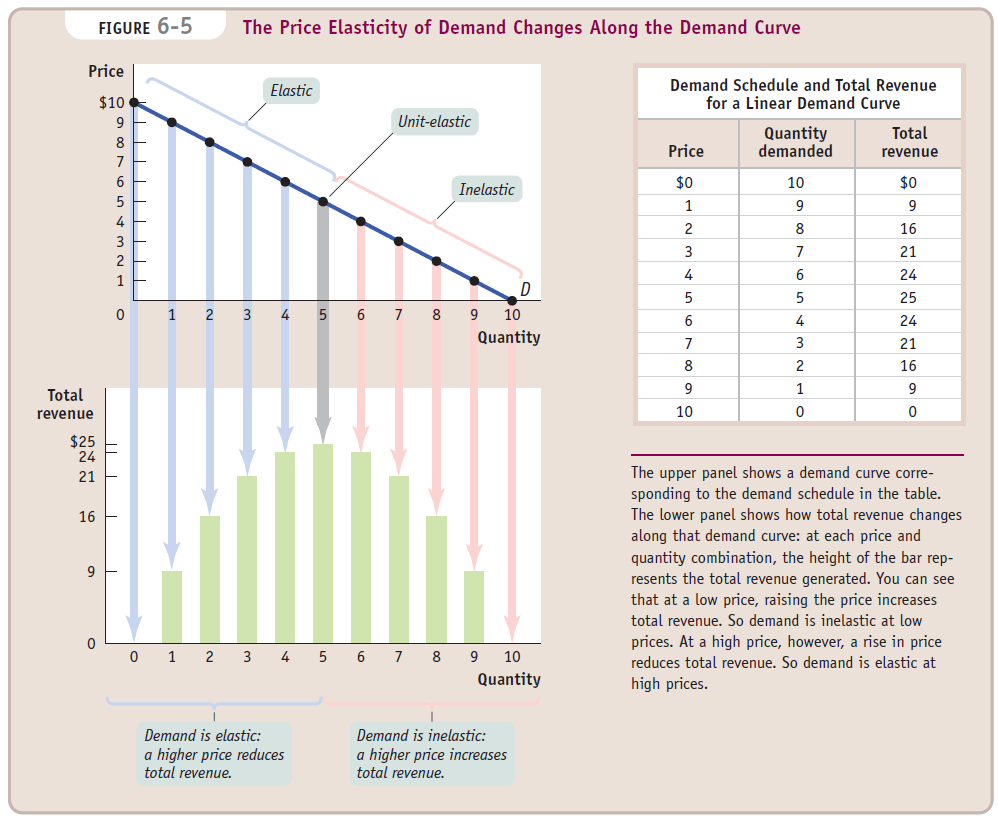

- The total revenue (total cost) remains the same when demand is unit-elastic

Question 8

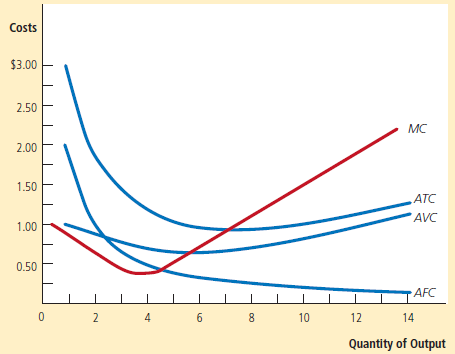

Average variable costs are increasing when marginal costs are higher than average variable costs

Question 10

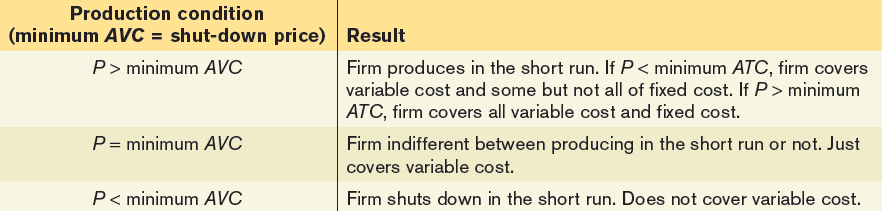

If price falls less than AVC, then you should shut down the company.

Long-run (Profitability)

Short-run (Production)

Question 14

Question 15

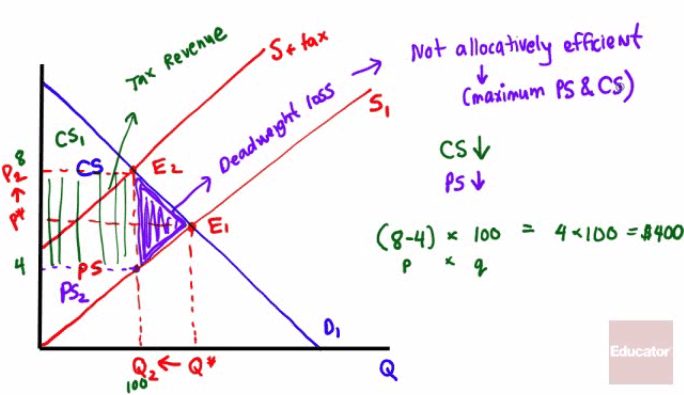

- Both consumers and producers bear a part of the total tax burden.

Question 17

Economic Profit = Accounting Profit - Opportunity Cost

In a perfectly competitive industry, the Economic Profit = 0.

So, Account Profit = Opportunity Cost